|

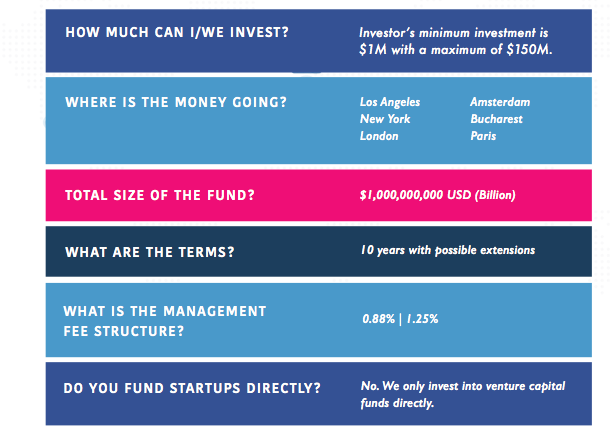

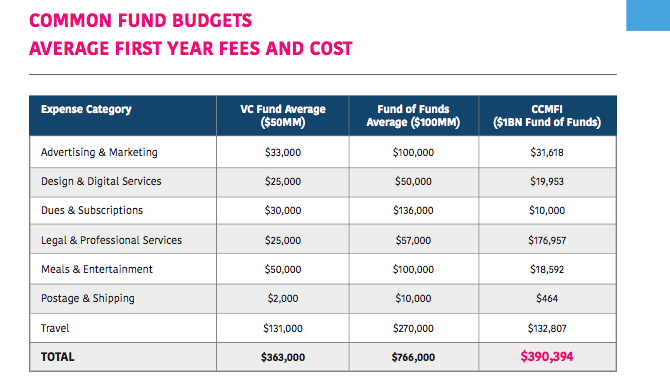

10/17/2020 The CCM UNFUNDFor every investor win, there is the one that got away or the anti-portfolio. That’s the companies that become publicly traded and when you had a chance to invest $10k in their angel round in 2012 or the startup you mentored and almost got a board seat on before your nemesis woo’d the founder away at the last minute. You think about it when you see the founder on TV or a family member buys you Earth-moo socks and you burst into tears “I could have gotten in PRE SEED!!!” Most successful investors always have a thing or two which becomes a big hit but somehow slipped away, for me, my anti-porfolio is myself and original batch of CCMFI VC investments. For me, the one that could have been, the one that got away, are the beautiful 2017 VC vintages CCMFI planned for that we had to change, modify, exchange, withdraw, whatever due to varying delays many of our Batch #1 VC selections. R.I.P Batch #1 I will always love you VC vintage 2017/2018. CCM Batch #1 (Planned 2018) ORIGINAL FUND DESIGN AND TIMELINES CCMFI founded from the earliest days a pension friendly fund-of-funds structure. Research began in August 2016 and by luck I came in contact with the Dutch government (in New York) who thought the fund-of-funds concept was clever for helping public funds make profits and be part of venture capital, which at the time would also be a publicity bonus for Netherlands as people were getting annoyed by slow innovation and flat returns on mandatory pensions. By March 2017 I was offered the idea of launching my new and upcoming fund FROM Netherlands as a win-win: I could save on setup costs, be near European pensions and Netherlands could get copies of my fund notes and learn from a Silicon Valley expert. Fair enough. I checked the market numbers and while similar to NYC market Europe had a massive amount of pension capital sitting in reserves with potential for growth so there was enough capital to indicate the venture capital market could reach 100BN annually. If you looked at the capital available to do so if even 1% of pension monies were allocated to venture capital, Netherlands could deploy $150BN assuming there was enough places for it to go (?).  While a tiny country in size, Netherlands is a serious global contender for capital reserves. See above. Looking at the venture capital numbers themselves, Europe was still emerging at CCMFI’s onset and showed itself on a trajectory towards $50BN+ annually. In 2017 EU venture capital appeared to be growing at a faster pace than NYC venture capital crossing over $25BN. See also The $50BN Elephant for a more detailed analysis.  After a few rounds of in person meetings with Netherlands on Third Avenue, including with my Board, I made the decision (albeit) quickly that I’d move to Netherlands and build my first-time fund from there. How my super early American LPs were okay with this I will never understand, I think everyone was curious how this would play out. Here is the letter they would later give me which would kickstart living and working in Netherlands. I was excited about it too it seemed Netherlands was loaded with potential. Note: If one of my fund managers lived in my hometown and said they were moving to a village in France where they knew not a single soul to launch a fund… I am not so sure if I am that brave. Not all heroes wear capes, Howard. CCMFI FUND TIMELINESMy original timelines with built in buffer for CCMFI had beta (American) LPs entering it May 2018 with pension enrollment around at the earliest 2019 (24-26 mos from april 2017), full close in 2020/2021.Like all funds, the more in placement I had the more I could capital call. I knew a 1BN fund would take time both oboarding LPs and executing safe investment deployments. The thinking, especially for pensions, was that the fund could operate and fund as quickly as possible while growing and maturing its product.   CCMFI FUND SPECSFrom the beginning of CCMFI there were fail-proofs or back up to backups to backups, which I would eventually have to tap into much to my amazement. All asset risk modeling I ran ended gave a minimum $1BN fund size and I was already getting feedback and documents from pensions saying diligence could take up to thirty (30) months and since there were multiple Dutch pensions with $100MM+ minimums and they could not individually be more than 20% of the fund, and collectively public pensions could not be more than 30% of my investor base, any FOF under $700MM in size simply would be too small. Fund Size: $1,000,000,000 USD Pension Timing: I figured this whole process would take 24-36 months from April 2017 a la pension friendly FOF deploying and calling pension capital as early as May 2019 and late as May 2021. I was also a first-time fund manager, a female, and with a thick American accent. I moved to Europe ready to GRIND not to be Emily in Paris. Investment Period: Since the fund started investing into VC funds in early 2018; with a three year investing window listed in the funds terms, this also meant any pension or LP delays could be met with one small extension with a small group LPs if needed. Short term this would be low on collecting income or management fees— long term useful to the fund’s integrity. At every fork in the road of this process I always opted for higher quality than quick or useless KPIs. In this way CCMFI is still within its original planned investment window until June 2021 assuming no extensions. Investments: Since commitments and capital calls are different timing altogether and each fund on its own schedule, the math between the GP and early adopters was tight so we figured out a way to keep certain VC slots or for no charge let cofunds or investors fill when appropriate. In advance I knew that patching fast-paced FOMO VC funds with incredibly slow turtle-power Pensions would be a challenge, so I came up with varying scenarios and would Side Letter or make different timelines for various VC funds. Shuffling time with venture capital funds was not too hard since often I was the lead or anchor and some emerging funds still had to finish raising their funds which can take a normal 1-2 years BUT the 2017/2018 vintage so lit even pulling in long standing favors there’s only so much time I would be able to buy on either side so the hard part would be filtering through hundreds of venture funds to find ones which could fit all of CCMFIs criteria and expediting and prioritizing them as fast as possible. Our Fund Strategy is online here over 1,600 people have found it so thats good. Investment Diligence: The hotter the funds I got into, the hotter my fund and there’s only so much FOMO pensions will eat they are not the normal LP who can be quickly coerced into a bowl of “fund is totally closing this week.” However I could do my best. See also Managing Venture Capital Relationships. We established hundreds of pages of documentation for our IVG group (VC investment review) sharing it all with Dutch pensions along the way. Everything from risk analysis to common foundation questions. I’ll email anyone a copy of our 2019 IVG group framework which is used by several of our co LPs if you send me a note. I can run the whole thing on one VC fund in a less than an hour if I do it myself, otherwise if followed it could take an junior analyst a few days / week to use to screen a VC fund. CCMFI INVESTMENT GROUPCCMFI Investment Group policies and diligence procedures (on VC Funds) - 36 pages  Want a copy of our 2019 IVG Documentation? Send me an email Low operating costs: Since pensions would be involved cost was always a factor. After review of legal, admin, operating costs I estimated that setting up a $200MM FOF would be about the same setup cost as a $1BN fund. CCMs budget for the fund setup estimated around $300,000 and the budget for the management company set arbitrarily to $700,000 (per year, and with no salary for myself). While LPs share Fund costs we knew early on the management company would take a few years to be profitable, which is normal for any new business. A new management company was in its earliest days and a new fund needed to be made for it. Since the whole idea of CCM is easy access for pensions, we also wanted to make sure costs were as low as possible and processes streamlined. From the data I have, I know that we built CCMFI for about the same costs as if a $100MM fund was setup and less in fees if managed in-house my someone. See also Managing Venture Capital In-House for other costs. Often CCMFI would / prefers to commit earlier to a VC to save on fees, any fees saved passed directly to pensions. CCMFI Fund costs are the far RIGHT column below:  OUR INVESTOR REQUIREMENTSBuilding a fund that gives preference to pensions is no easy feat. Armed with a general manifesto for venture capital investing and penchant for pensions (see also, The People’s Money) there were additional considerations about who could be an LP and how many which all had to be planned out in ADVANCE to the fund’s various documents and rules being made like LPA. On the surface the main components for LP demographics worked as such:

NETHERLANDS SO NETHERLANDS Snapshot from Michelle Buteau's Netflix special, Buteaupia. Also current mood With a fund roadmap in hand, I began building my first fund in a faraway land, living mostly off the caffeine of free office coffee and Stroopwaffels. First CCMFI beta LPs came in May 2018 as scheduled and I REALLY knew by February 2019 that a June 2019 (earliest entry date for pensions) would not work since we were still awaiting approvals on various documents from that were submitted the winter before looking to be approved but pending. The corporate LPs were behind the pensions with DDQs falling behind. Without much choice I had to start changing many VC positions in 2019 and changing a super-well-thought-out-plan for investments and LPs to allow other funds to move forward at a faster pace because I could not reduce the quality of the fund. See also You Cannot F**king Ship a fund. I kept trying to convey the urgency in Europe realizing CCMFI needed to be ramped up for a fall 2019 pension onboarding to assume it would take some months, yet everyone was getting ready for European "holidays" while the American VC funds and startups were building (like all thru every night Europe slept) and their valuations were skyrocketing quickly as they should. Since this growth pattern doesn't exist often in Europe its hard to explain to someone who hasn't seen it themselves. I will always love you VC vintage 2017/2018!! (Batch #1) Planning to move around VC positions is stressful and some funds I had found in the deepest corners of the earth or competitively gotten in --I would find many VC funds new LPs to swap CCMFI out. Sometimes you gotta do what you gotta do and I’m lucky to have gotten into that vintage at all, but never again will I do so much work “for free” and I mean that towards pensions too. There's hundreds of venture capital funds in the world but Batch #1 is still the one that got away. That combo. That timing. Those market conditions. Those exact startups, sigh. Another strange thing in Netherlands was that after successfully passing a fairly large EU diligence packet—some bad actors started to pop up, Dutch vendors began to overbill the management company, the Dutch government “coincidentally” entered me into an audit immediately after and withheld the renewal of my residence permit until the audit was done with a reminder that if I left Europe I would not be allowed back, and— It felt like everyone knew my fund was moving forward and wanted a “cut” even though I was only halfway there and a few million deep in expenses (already) and no paycheck (yet). IF YOU SAY THE WORD ROI ENOUGH TIMES...Other quirky things had popped up, I remember being covered in shingles once from stress, while in hour 34 of a 100hr pension compliance packet (DDQ in Dutch) and walking by the office lobby to see a Dutch prince talking to a startup about how to get app users with “ROI” sewn into his jacket; meanwhile I couldn’t find a single person in the building who either knew Dutch well enough or knew venture capital well enough to help me with various forms. I promised myself and the government of Netherlands two years minimum and I am generally a person of my word, but every single DAY after two years passed (formally July 2019) I kept asking myself: why was I trying to do this fund from Netherlands... if another European country be any better... and what was I trying to prove? I might as well have been in outerspace: I felt like a female Matt Damon trying to grow potatoes on a space planet which had been beaming signals across the universe that it wanted venture capital for lightyears but really it just wanted my potato seeds and spaceship. I kept hosting several hundred person VC nights in Amsterdam and Zurich with many pop ins to Romania and aside from my former Associate, George Moroainu (who is killing it in Romania having just closed a Seed Round and recently surpassing 1.3BN Euros in sales for his startup post CCM) most the European CCM interns or employees I poured my heart and soul into training ultimately went to safer, easier jobs in academia or banking. Turns out doing Silicon-Valley-style-fast-deals from Amsterdam is actually stressful to most Europeans not a selling point. AMERICA SO AMERICAOn the flip side for every issue related to the lack of venture talent in Europe there was the issue of abundance of venture knowledge in the U.S and a stereotype that usually follows that which is white-dude-greed. I even had an American guy (former Citibank employee, so he should know better) demand more than $200,000 (for a harddrive of data stolen from my fund) paid to him tax free otherwise he would leak a bunch of information about myself and my fund in a way that would be detrimental. Not only did I not cave in but I couldn’t have anyway from Money laundering (AML) polices in place to protect our future pension LPs—as a fund every penny would be counted how could I justify such a payment which would be clearly recorded? I didn’t cave in to the demands so its no surprise what happened next. MEDIA HITPIECE This is the cover image of the article showing mostly men hanging around and drinking with the few females in the photo being subservient or preyed upon. The article shared identical framing spending pages connecting dots from stolen data into a larger over-arching fabrication construct meant to sabotage CCMFI at exactly the right at a time when pensions were scheduled to be entering my fund. One could argue I was Tonya Harding-d, clubbed before I had even spread my wings. A couple talking points related to that article for anyone who has read it:

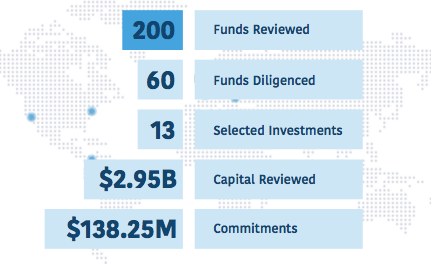

ENVIRONMENTAL CONSIDERATIONSWith or without the takedown piece which seemed to only slowly be shared around Europe, there were several environmental factors putting my fund at risk by being in Europe I started to notice more and by March 2020 when all the various country borders locked down. I had months to think about this before deciding to move back to the United States which I did this August 2020. Here are three market components I felt would make it impossible to STAY in Europe if I wanted to continue running a fund-of-funds or even stay in venture capital (aside from even Covid-19 or personal reasons): EUROPEAN GROWTH NUMBERS INACCURATE(LTV, Long Term Value, not high enough) By the time I discovered it in March 2020 it was almost too late to move back to the U.S because all country borders were closing but it was clear—most of EU venture capital was American money taking advantage of low startup valuations. The American capital which was more than 50% of Europe annual VC #s was also forcing European startups to setup American LLCs to accept the cash, so the money might have been arriving in Europe via America but it was going right back. It also explained why there was such a small startup workforce and starter founder ecosystem on the ground, particularly in Netherlands. I had a very promising Dutch kid I poured a bunch of knowledge and resources into and a year later he hadn’t absorbed most of it, one of the last times I was in the Amsterdam office he asked me if I knew what a “termsheet is” he said “you know for startups…” I run a fund based whose underlying assets are completely on capitalization tables and startup termsheets and that was the core to everything I had been teaching him #NEXT. CAPITALISM DOESN'T WORK IN EUROPE(TAM, total addressable market too small) While venture capital is an asset class and tool for empowering young and high growth companies in the private sector, its mixes well with public pension funds getting access to private profits, the base of venture capital is CAPITALISM. Fruit of thy labor. Eye for an Eye. Work hard, make money. Most of the philosophical concepts powering capitalism do not apply or wont stick in Europe. Firstly, European culture does not reward risk or entrepreneurism. Most of the wealth in Europe is from old old old money, likely linked to castles and devastating an entire village (Side note: my college dissertation in college was on inheritance within capitalist societies). Secondly, services in Europe cover most people so that they are not encouraged to think or act professionally outside of the box, everyone is well cared for. When you combine the two factors of old money and social services you end up with a very rich class of people (“Why would I invest into venture capital to become MORE RICH? I’m already rich” one EU family office once told me) who have no incentive to invest into venture capital and the concept of even wanting or desiring to become rich not common amongst the rich or those in middle or upper clasSes. In America and other countries an entrepreneur who makes their own money is respected however in Europe no one seemingly cares as everyone has their own socially protected life to live. This also seeps into business hours, work ethic, work timing and all other pieces to a puzzle needed for building “rocketships.” How can venture capital be on the rise and “exploding” in Europe if there also no whole set of founders ready to build? Venture capital is a SPORT as much as its an asset class and the love for the game the way it exists in the U.S simply does not exist elsewhere in the world #AMERICA GREED (NOT MINE)(CAC, Customer Acquisition Cost too high) As soon as my fund started ramping up traction we had issues with local greed in Europe and people’s expectations that since CCMFI was meant for pensions that somehow money could be wasted / shared. Not true. We had American and Dutch shakedowns with a couple still pending however, for the amount of effort it takes to get even 1 LP in Europe I could have gotten 4 in the U.S. Both sides have their own ways of expressing greed so I pick the one with higher ROI for the hassle. ~THE CCM UNFUND~Even in hindsight and the things which were in my control I’m not sure there is much I would have or could have changed for CCM’s launch. I think even if I had hired a European grown General Partner, there would have been slowness. I think even if I had caved in and paid off blackmail payments, only more blackmail requests would surface. And I think even if the market data for venture in Europe was more clear that it was mainly (almost entirely) overflow American capital, I still would have gone out there to check it out and see how “emerging” its emerging market is.That said, it’s a pity things could not have launched even two months sooner because I’ve had parking spots in VC funds that have been investing in startups since before 2017. Here is where CCMFI would be today had we even remotely followed our launch schedule: the fund would have launched and deployed $100MM by now, with 3x-5x in performance (and growing, some positions are known to already be performing in top percentile internationally) and over 20+ VC LP positions. Assuming LPs entered CCMFI at their projected order that would have put the first pension into the fund June 2019. While Batch #1 CCMFI funds is almost entirely different today that selected back in 2018, part of it is still my anti-fund and group of talented people I will watch from afar hoping for any chance to support them--once you bet on someone professionally its heartbreaking if your timing fails but it doesn’t change conviction. If Batch #1 had gone to schedule that would have put CCMFI as a top fund in the U.S and world. While starting up I met a half of dozen funds like mine scheduled to be $1BN or more so this size will be common. CCMFI was very forward thinking in its creative structure and ambition which I hope never goes away, despite the bruises. If CCMFI fully closed last year (not planned) it would have been top in size for Q3 2019, if CCMFI ever reaches $1BN this would be new pack of kids at school.  Batch #1 going seamless would have also put CCMFI #1 for deals done since we had 13 positons allocated in September 2018.  MY RISK MY EXPENSEOn a personal level and having mainly missed the projected window of my fund’s Batch #1 launch, I lost out on American income during this time for around $1MM ($250k X 4yrs = $1MM), and fund expenses paid back of $300,000, any type of income for running the fund (anywhere from $200k a year to $500k a year X 2 years = $400k - $1MM) EUROPE AND DELAYS = $1.7MM to $2.3MM lost income Personal income loss aside, I have never worked so hard in my life to get placement, move placement, help placement, build out a robust and strong backend pensions could trust and essentially doing this all from a strange place with minimum resources at hand. I certainly took some short term loses building a fund from the ground up which is normal for a GP, and the fund itself is performing well considering it all, so even if CCMFI makes up time or launches a new fund, or deploys Batch #2 to VCs quickly… whatever we do it I will never having those Batch #1 vintages and positions in that combination and no markup again. Batch #1 will always be the ones that got away, who I love from afar, my anti-portfolio, the glass stepped on at a Jewish wedding marking both that things will never be the same and never can be. I have very fond memories for my experiences living and working in Europe now that I'm back in the States. Some of those times were sweet and endearing, other parts I learned about myself and expanded in ways I didn’t think I should. But if you ask me if I still like Stroopwaffels, the answer is no. ============ ABOUT ME: Venture capitalist having worked San Francisco, New York, Bucharest, Amsterdam, and Zurich. I spent the last few year building an awesome fund-of-funds. For more follow me on Twitter @ecachette or visit elliecachette.com ~~~SOME DISCLAIMERS~~~

CITATIONS AND BACKLINKSIMAGES

LINKS AND RESOURCES

Comments are closed.

|

common tags |

RSS Feed

RSS Feed