|

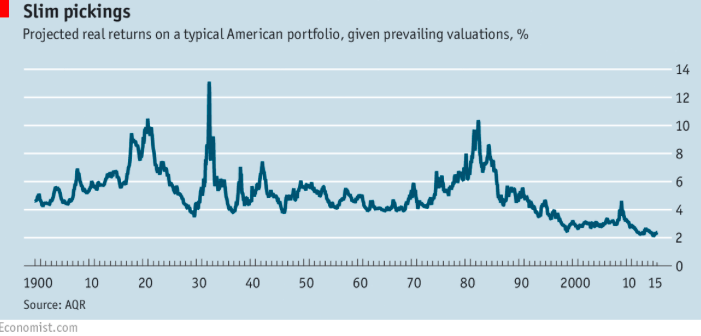

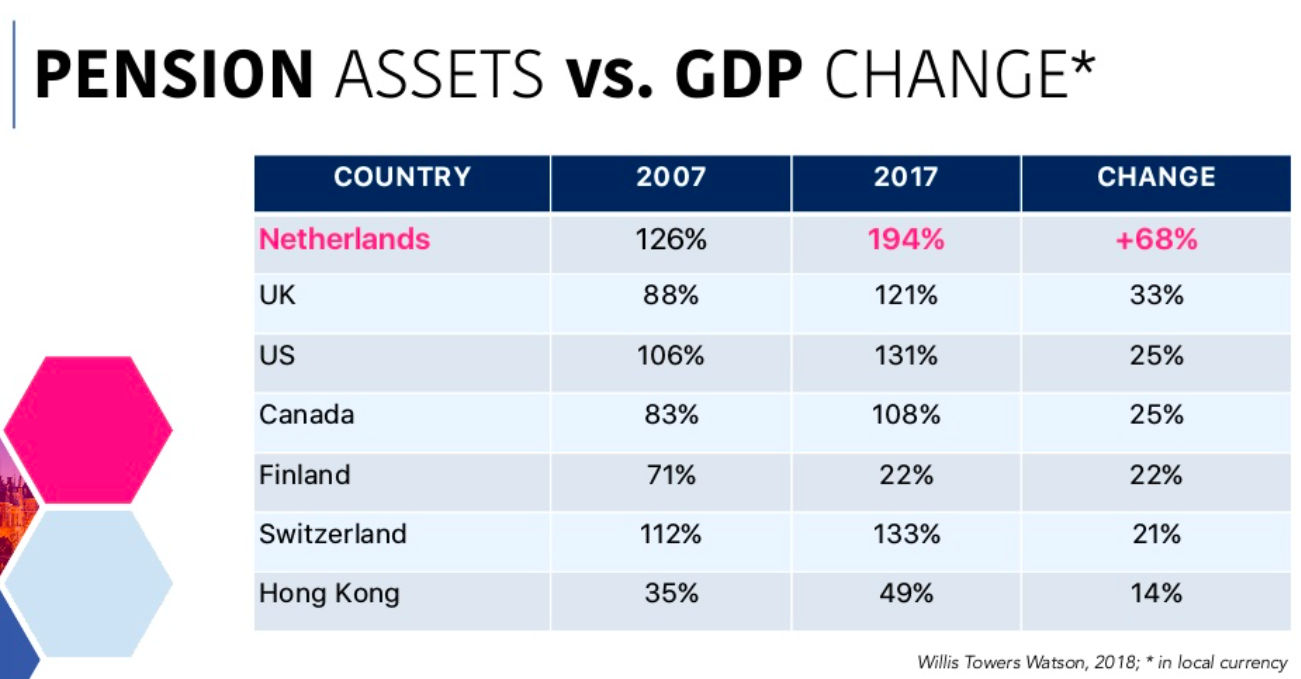

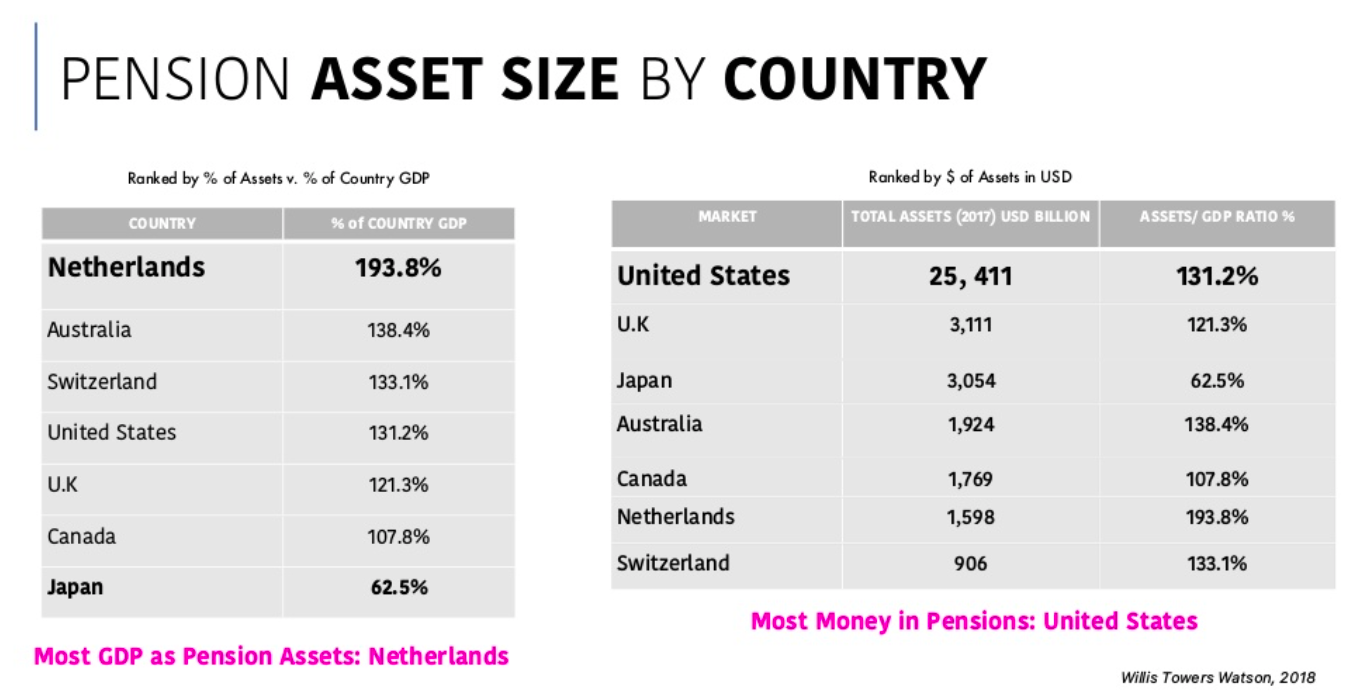

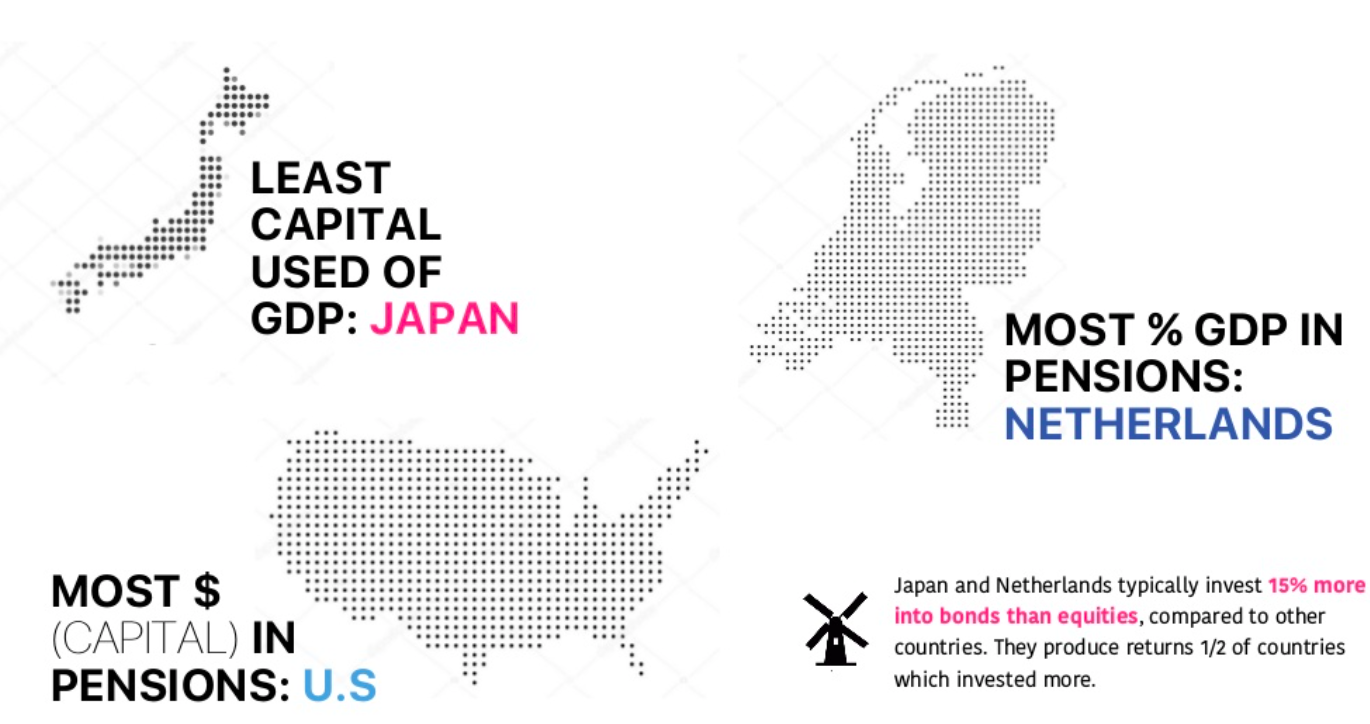

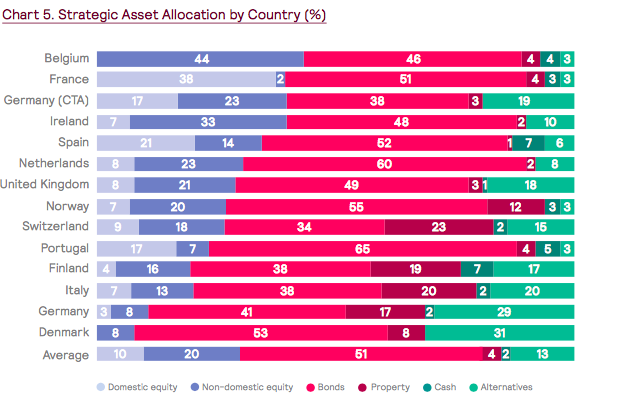

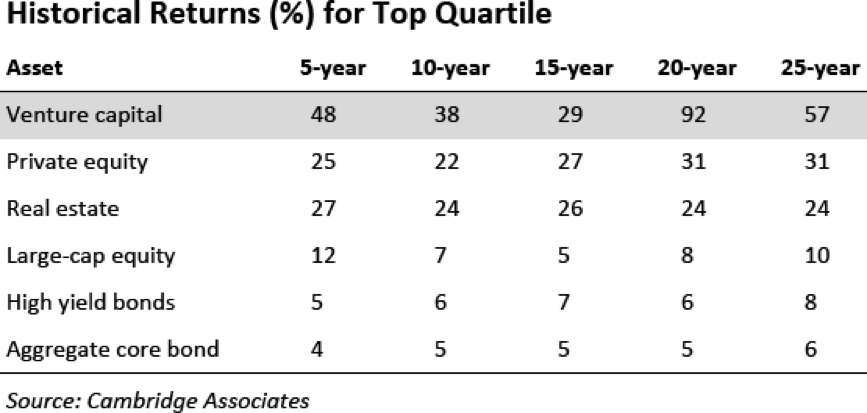

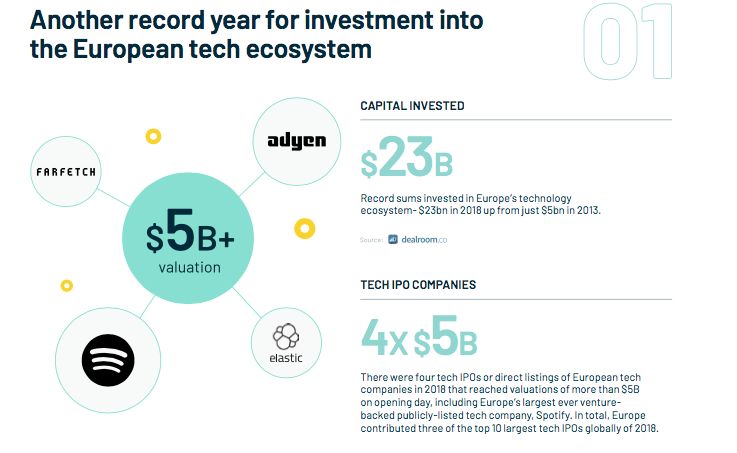

12/18/2018 Venture Capital: The People’s Money My understanding for a while was that venture capital was funded mostly by rich individuals, it wasn’t until later on in my own professional journey that I learned more about the origin of venture capital, namely, that large pension funds were much of the investors behind venture capital funds. In the U.S this is more commonplace and has been for some time, in Europe this is becoming more mainstream as well but only recently. What has started to strike me as odd, is that consumers are always paying the costs for things without having many business rights. What I mean is that consumers work hard for their money, are often forced to contribute portions of their pay into pension funds (which may or may not produce returns) then buying for goods which is also form of investing. If you look at Tesla they are a perfect example where there have been government subsidies (funded by consumer's taxes, and later paid off wth consumer money from revenues), then consumers often pay in ADVANCE for a product which doesn’t exist yet (free business loans without any equity) and then, using post-taxed money they can have the ability to buy publicly traded stock into the same company, while also paying sales taxon the price of said cars. Huh? Let's not even go into lack of Tesla transparency and ranting tweets earning SEC fines which ultimately are passed along to shareholders aka consumers. The world is shifting and consumers are now the ultimate investors and starting to realize such, this is why we see the rise of crowdsourcing platforms, Kickstarter campaigns and GoFundMe’s. People are hungry to find a way to leverage collective power, when really, they’ve had it the whole time. WHEN SAFE INVESTING ISN’T ENOUGH Now the problem and the beauty of pension funds investing into things is that it’s a great way to pool together (“the people’s”) resources and make bigger decisions for the collective good. In theory, this is a great way to accomplish a lot. One of the challenges these pensions are steered towards “safe” investment allocations only to find that people are living longer, more dividend returns are needed and thus the “safe” model is starting to hurt the banks and people who rely on their dividends later in life as the bar for performance continues to rise. Sometimes it goes bad too, I’ve had relatives lose much of their pension monies from mismanagement so pensions as it turns out, from a consumer perspective can often be a greater risk to cash flow. Looking at the fundamental structure of pensions, the life expectancy of a human back in the 1960’s was something around 52 years old, followed by a spike and by 1970’s the average life expectancy was 67.1/74.7 (male/female). Given technological advances and trends in science this number is already believed to be past 80. If pensions were designed as a safe way to save money, how can the same fund investment structures that were supporting those with the average lifespan of 52 somehow also perform for those living to 80? It’s impossible. That’s doing the same exact thing expecting an outcome needed to increase profits by 0.65x. How? Pensions will be forced to change their asset allocations and investing strategies or risk becoming extinct. Let’s take a look at overall American pension performance:  Economist, 2015 This lack of performance is not only from too conservative of investing approaches its also from the increased life expectancy and needs / dependents on the funds. Besides the obvious lack of performance this is also an opportunity cost for the people, as these funds could have been applied elsewhere for better returns. Produced more jobs or more profits, lots of opportunities missed. There is also similar data with GoLocalProv in a fascinating report Riley: Effect of Insider Politics on RI’s Pension Fund Under-Performance Now let’s look at where a lot of this global pension capital is and who the major global players are in the game of pensions:    (Data courtesy of Cachette Capital Management. Full presentation can be found here on Slideshare) If we dissect and look at the typical breakdown of pension asset management capital is usually spread across asset types like bond, equity, property, cash and alternatives:  This full report with the above can be found here by the FCHub, Financial Community Hub, there are many resources online citing the same breakdowns. The interesting thing here is that venture capital is still not considered equity. Venture capital usually falls within "alternatives" and is competing against many other forms of "alternative" assets. If we look at the top countries with capital in this chart namely Netherlands, thats about 8% total for alternatives and venture is less than 1% of that 8%. Yet if we look at the typical returns of these asset classes we see a totally different order:  So, what is going on, if we know that venture capital could be a great tool or asset class why isn’t there more pension involvement in venture capital? Well it turns out logistics. TIME FOR INNOVATION While U.S pension funds slowly address venture capital opportunities, some countries are ramping up to quickly overhaul their current investing practices. Understanding that the current investing strategy doesn’t work to maximize capital, it’s starting to make sense to actually put the people’s money to work. In France there’s the expectation that over 1BN in capital over the coming years can be applied across startups and venture. In Netherlands there’s a whole initiative being rolled out across the Pension federation around not only venture capital, but innovation and social responsibility and if there’s any country to move the global needle in pension-venture capital investing its Netherlands. With Trillions in capital that could be put to work (Netherlands alone), even if asset allocation was increased to be say 3% of the current models to be venture focused, that’s billions to fund upcoming startups, ideas which consumers like, or fund things that might change the world altogether. Since pension money is the people’s money after all then it would make sense to shift towards market demand and yet we see even more interesting things happening in Europe around pension investing. Penseon Federation (November 2018) in its additional referendum for investing. Full memo can be found here: Dutch (original text): "...verwijzing opgenomen naar informatie over de omgang met maatschappelijk verantwoord beleggen" English translation: reference to information about the management of socially responsible investing This is quite interesting, for a nation loaded with capital (Netherlands) which can be put to use, its already outlining framework for socially responsible investing, yet wouldn't venture capital be considered a socially responsible way to apply funds on behalf of the people? Not exactly but also exactly. THE CHALLENGE: EXPERTISE The other challenge with investing into venture capital is inherently not a pension and vice versa. The skills for venture capital are completely different than that of a huge public fund. There is also the issue of potential fraud or bad investments, which is why many pensions across the world have “minimum” commitments of $25MM or $50MM or $150MM for underwriting purposes. There needs to be verification, investigation, and diligence. For the pensions aka “the people” to pay for this time it has to be worth it, as in worth the investment size. Mathematically when a pension fund is somewhere between 100BN and 300BN, the investment size (into any asset class) should also be notable enough to matter, to even move the needle. What’s the solution here? Well as it turns out there is a mechanism already in place that fits this, it’s a Fund-of-Fund. An investment fund which invests into many funds, which traditionally would have been hedge funds or bonds it’s become more acceptable (and it makes more sense as the asset class stabilizes) to see fund of funds specifically set for venture capital. Streamlining investment money into venture capital but spread across dozens of VC funds makes a lot of sense but there are not many FOF’s like that… until recently. There are more venture capital funds than ever before in history. In the US alone there were over 400 sub-200MM venture capital funds launched in the last two years and while the number of European VC funds is not exactly known, new and more funds that are even smaller launching is possibly a good thing, it also means there more venture capital talent working specifically in venture capital and not at pensions or fund of funds. A FOF for venture capital would not be for the lighthearted: the responsibility astronomical, expertise across every area needed: legal, asset management, knowledge of underlying assets (startups) and how to properly manage each piece of the supply-chain. CONSUMERS AS STAKEHOLDERS If consumers are the investors and stakeholders behind pensions, shouldn’t consumers have more say in where this pension money is applied? Unfortunately they aren't even in the conversation. How pensions make their investment decisions comes largely from institutions or managers already getting well paid by management fees with zero incentive to increase risk or invest into other areas. Yet if we look at the stability of venture capital; since the 1980’s venture capital has started producing returns anywhere between 2x and 15x and it’s not without the consumers either: they have been using and investing into new products, new companies, trusting startups to do things like pick them up in cars (Uber) who go on to become publicly traded companies. Venture capital is becoming successful because of consumers, and it’s this use and investing with post-tax dollars that make it a shame for them to not have more equity. Its rumored that Europe has more billion dollar companies in the lined up under venture capital than ever before and the trend is showing no signs of slowing down. Its rumored that Europe alone is hiding dozens of billion dollar companies ("unicorns") who are producing revenue and scaling globally.  Atomico's State of The European Union Report (December 2018) A copy of the full report can be found here.

For the big question: why aren’t pensions following more of what its constituents need, want, use and have-to-have? Why are pensions still investing less than 1% of their allocation to venture capital when 1 in 3 consumers are using products which were at some point backed by venture capital? Why don’t consumers have more of a voice? Well, they do its just used in the wrong directions. It’s only a matter of time that consumers not only vote with their currency (buying things) but that they demand too their pensions work for them. WHAT THIS MEANS FOR THE PEOPLE The good news in all this shifting is that people are going to start getting a bit more of what they deserve. Products and startups already do and will continue to see cheaper setup costs, pension funds more likely to produce better returns and supply the dividends promised or more and the enlightened consumer will have more input into the things they use and the things which become successful. So while kickstarter campaigns and crowdsourcing is surely not to go down anytime soon, we should see the people’s money being put to work and doing good, for the people. The whole world and how it invests is already changing: entrepreneurs are going to become VC Fund managers, VC fund managers are going to become FOF managers, FOF managers are going to start working for the banks directly and in all this movement it’s a good thing because it means more knowledge will be spread across the lifecycle of venture capital and with VC as an asset class stabilizing. We can also be sure over the coming decades that venture capital is soon to be the new Private Equity. More than all that, how powerful is it that the future is not only going to be funded by the people but decided by them too? Venture capital is the new private equity and consumers are the new investors. ABOUT ME Founder at heart I’ve spearheaded startups, consulted for VC funds and now the fearless leader of a global fund-of-funds investing into early stage venture capital funds. If you have an interesting VC fund or would like to know more send an email to ELLIE (at) CACHETTECAPITAL (dot) com. Comments are closed.

|

common tags |

RSS Feed

RSS Feed